Fraud is a phenomenon that has been in existence since the beginning of time. It still continues to plague the world now. Fraud is “generally referred to an act of deceiving illegally in order to make money or obtain goods.” In the past decade, there has been a steady upsurge in the cases of financial fraud that have been reported in India. It is important to note that financial fraud is seen as a part and parcel of the business world. Especially, post the liberalisation of the economy. But the steady upsurge in cases of such financial frauds, and the fact that the complexity of such frauds has also been increasing. This poses some serious issues for the regulators of the financial institutions.

In India, the banking sector is mainly regulated by the Reserve Bank of India. They have defined fraud as “A deliberate act of omission or commission by any person, carried out in the course of a banking transaction or in the books of accounts maintained manually or under computer system in banks, resulting into wrongful gain to any person for a temporary period or otherwise, with or without any monetary loss to the bank”.

The Ketan Pareikh Scam (2001), the stamp paper scam (2003), the Satyam Scam (2008), Vikram Investments Scam (2018) are some of the biggest cases of financial fraud that have happened in India in the last two decades. These scams involve huge sums of money, which is a great loss to the country. As per the “Financial Stability Report by RBI released in the month of June, in the year 2018, the banking system has reported around 6,500 instances involving fraud of around Rs 30, 000 crores in the last fiscal year.”

The “Indian Penal Code of 1860” is the primary statute that governs criminal offences in India, and the procedural law for the conduct of proceedings is prescribed by the “Criminal Procedure Code of 1973”. In addition to this, there are provisions of the “Companies Act of 2013” that provide provisions to curb fraudulent activities in companies. “Section 447 of the Companies Act is one such provision whereby fraud is defined as including any act, omission, concealment of any fact or abuse of position committed by any person or any other person with the connivance in any manner, with intent to deceive, to gain undue advantage from, or to injure the interests of, the company or its shareholders or its creditors or any other person, whether or not there is any wrongful gain or wrongful loss.”

“The Prevention of Corruption Act 1988 and the Prevention of Money Laundering Act 2002 were some enactments that were made in order to deal with the issue of corporate and business fraud.”

Technological advancement has given rise to some new types of financial fraud, and the same have been listed hereunder:

Phishing – In this type of financial fraud, the fraudster targets the internet banking clients by sending them tricky emails that would ask for the person’s account details to a website that would look like a legitimate website of the concerned bank.

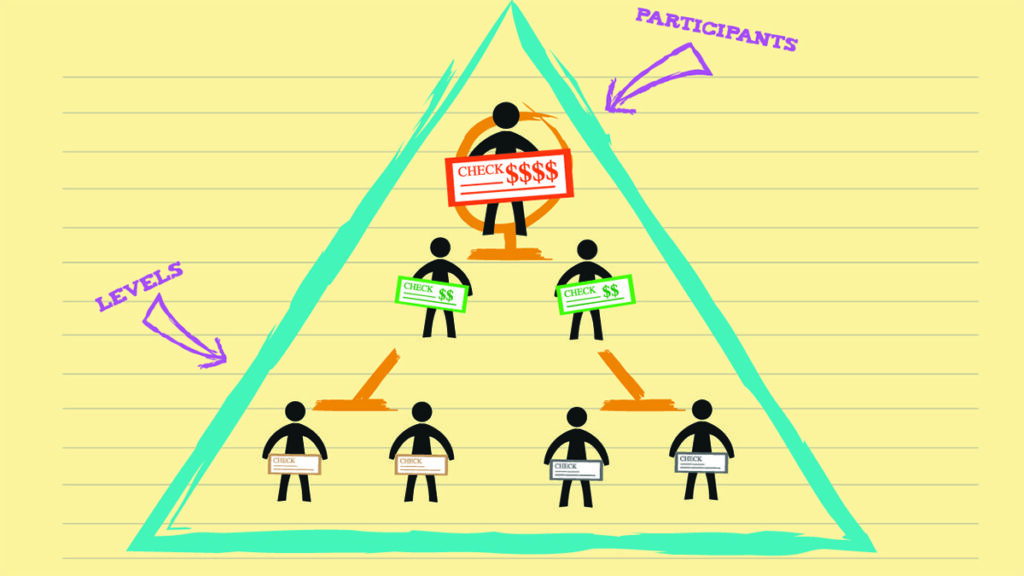

Pyramid Schemes – This type of financial fraud refers to a system that guarantees the customers or financial specialists enormous benefits that are based on the recruitment of others to join their program, not founded on benefits from any genuine speculation or genuine offer of merchandise to people in general public. A few plans may indicate selling an item, yet they regularly basically utilise the item to conceal their pyramid structure.

Skimming- Under skimming, the fraudster usually steals information from a credit card by using a wedge or any other form of a skimming device that records all the information on the magnetic strip when a person swipes or uses his/her card for a proper and legitimate transaction.

Identity fraud- This type of fraud refers to a person wrongfully gaining an individual’s personal information and then using the same to rob the person of their money.

Advance Fee Frauds- These tricks are typically executed through a letter, email, or call offering whereby the fraudster offers the victim an enormous amount of cash on the condition that the victim can assist somebody with moving a huge amount of rupees or other money out of their nation. To start the exchange, the victim is solicited to send subtleties of their financial information and an organisation fee.

It is important to note that the aforementioned list of financial frauds is not exhaustive and does not cover all financial frauds. There are more types of financial fraud that exist in the country. But a common feature that was observed while researching the aforementioned types of financial frauds is that in most of these frauds, the fraudster has contacted the victim through the internet and has attempted to make use of the advancement of technology, such as credit cards and other mobile banking features that have evolved in recent times.

The “Information Technology Act, 2000” was enacted by the government to deal with the issue of fraud committed via computers and cyberspace. Section 43 of the aforementioned act provides for damages up to ten lakhs. This is payable by the wrongdoer to the individual influence on the off chance that there are unapproved acts submitted in regard to someone else’s PC framework like accessing, downloading, or making duplicates of the data or information stored in their respective PC systems. Further, the said Act likewise provides for disciplinary detention up to three years for messing with the PC source code and for hacking the PC frameworks.

It is important to note that there is no separate legislation that deals exclusively with the issue of such financial fraud that is committed in cyberspace. It is important for the government to enact suitable legislation in order to keep up with the changing times and curb the increasing cases of such financial fraud.